How Does Compound Interest Work? The Complete Guide (2026)

What Is Compound Interest?

Compound interest means your interest earns interest. Each time interest is calculated and added to your balance, your new balance becomes the base for the next calculation — creating a snowball effect that accelerates over time.

Definition: Compound interest is the process of earning interest on both the principal (your original deposit) and the accumulated interest from previous periods. The result is exponential growth rather than linear growth.

Here is the simplest way to understand it:

- Year 1: You invest $1,000 at 10% → earn $100 interest → balance is $1,100

- Year 2: You earn 10% on $1,100 (not $1,000) → earn $110 interest → balance is $1,210

- Year 3: You earn 10% on $1,210 → earn $121 interest → balance is $1,331

Each year you earn more interest than the year before — without adding a single dollar.

Use our Compound Interest Calculator to see exactly how your money grows.

Compound Interest vs Simple Interest The Key Difference

Most people learn about simple interest first. Here is how the two compare on the same $5,000 investment at 8% over 10 years:

| Year | Simple Interest Balance | Compound Interest Balance |

| 1 | $5,400 | $5,400 |

| 2 | $5,800 | $5,832 |

| 3 | $6,200 | $6,298 |

| 5 | $7,000 | $7,346 |

| 10 | $9,000 | $10,794 |

| 20 | $13,000 | $23,305 |

| 30 | $17,000 | $50,313 |

With simple interest you earn the same $400/year forever. With compound interest, your earnings grow every single year. After 30 years, compound interest produces $33,313 more on the same $5,000 investment.

| Feature | Simple Interest | Compound Interest |

| Calculated on | Principal only | Principal + accumulated interest |

| Growth type | Linear (straight line) | Exponential (curve) |

| Common use | Short-term loans, car loans | Savings, investments, mortgages |

| Formula | A = P × (1 + r×t) | A = P × (1 + r/n)^(n×t) |

| Better for borrowers? | Yes | No |

| Better for savers? | No | Yes |

The Compound Interest Formula Explained

A = P × (1 + r/n)^(n × t)

Breaking it down:

| Variable | Meaning | Example |

| A | Final amount you end up with | $14,025 |

| P | Principal — your starting amount | $10,000 |

| r | Annual interest rate as a decimal | 0.07 (= 7%) |

| n | How many times interest compounds per year | 12 (monthly) |

| t | Time in years | 5 |

Example: $10,000 at 7%, compounded monthly, for 5 years:

A = 10,000 × (1 + 0.07/12)^(12 × 5) A = 10,000 × (1.005833)^60 A = 10,000 × 1.4176 A = $14,176.25

You earn $4,176.25 in interest without doing anything extra.

How Compounding Frequency Affects Growth

The more often interest compounds, the faster your money grows. Here is $10,000 at 6% over 10 years with different compounding frequencies:

| Compounding | Times Per Year | Final Balance | Interest Earned |

| Annually | 1 | $17,908.48 | $7,908.48 |

| Semi-annually | 2 | $18,061.11 | $8,061.11 |

| Quarterly | 4 | $18,140.18 | $8,140.18 |

| Monthly | 12 | $18,193.97 | $8,193.97 |

| Daily | 365 | $18,220.39 | $8,220.39 |

Daily compounding earns $311.91 more than annual compounding over 10 years on the same $10,000. The gap grows larger with longer time horizons and higher rates.

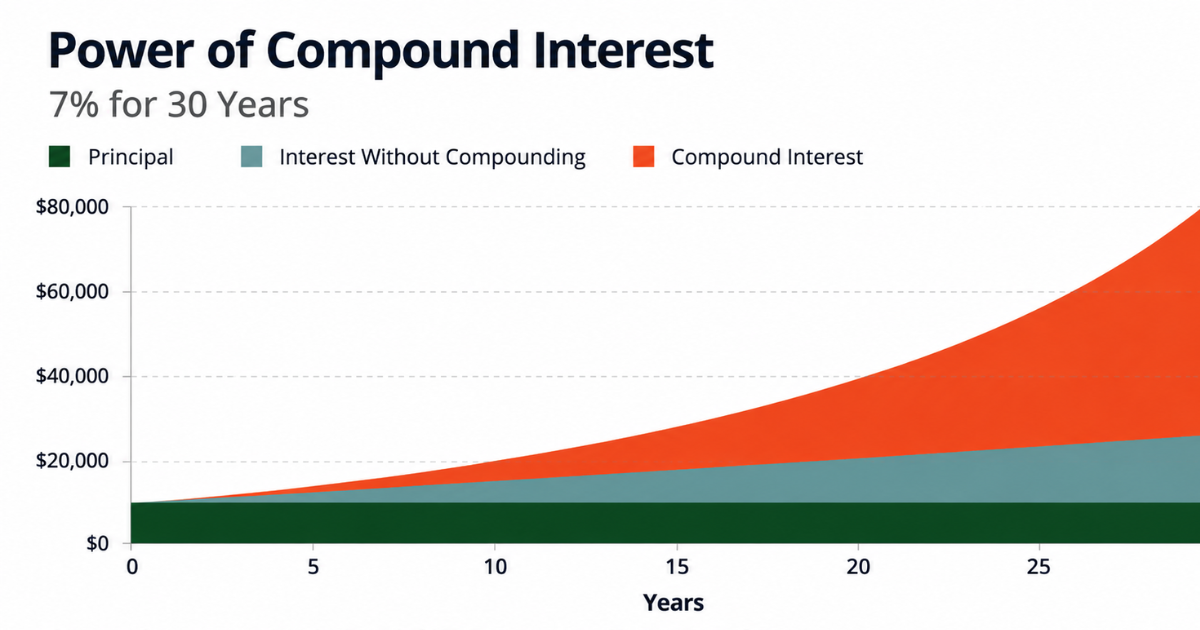

The Power of Time Why Starting Early Matters

Compound interest rewards patience more than any other factor. Here is how much a single $10,000 investment grows over different time periods at 7%:

| Years | Final Balance | Total Interest |

| 5 | $14,025 | $4,025 |

| 10 | $19,672 | $9,672 |

| 15 | $27,590 | $17,590 |

| 20 | $38,697 | $28,697 |

| 25 | $54,274 | $44,274 |

| 30 | $76,123 | $66,123 |

| 40 | $149,745 | $139,745 |

Investing for 40 years instead of 20 years does not double your money it quadruples it. This is the exponential curve at work.

The Cost of Waiting 10 Years

| Investor | Starts at | Invests | Rate | Balance at 65 |

| Early | Age 25 | $10,000 | 7% | $149,745 |

| Late | Age 35 | $10,000 | 7% | $76,123 |

| Difference | — | Same $10,000 | Same 7% | $73,622 less |

Waiting 10 years costs $73,622 on the exact same investment amount. Time is the most powerful variable in compound interest.

How Compound Interest Works Against You Debt

Compound interest is powerful for growing savings, but it works the same way against you when you borrow. This is why credit card debt can spiral quickly.

Credit Card Example

You carry $3,000 in credit card debt at 22% APR, compounded monthly, and make only minimum payments of $60/month:

- You will pay approximately $3,285 in interest before the debt is cleared

- It will take roughly 8 years to pay off

- Your total payment will be over $6,285 on a $3,000 balance

The same compounding math that builds wealth in savings accounts accelerates debt when you are the borrower.

Use our Loan Compound Interest Calculator to see how quickly debt compounds.

Compound Interest in Real Life Where You See It

Where compound interest HELPS you:

- High-yield savings accounts (HYSA)

- Certificates of deposit (CDs)

- 401(k) and IRA retirement accounts

- Index fund investments

- Dividend reinvestment plans (DRIP)

Where compound interest WORKS AGAINST you:

- Credit card balances

- Personal loans

- Student loans (if interest capitalizes)

- Payday loans

- Buy now, pay later (BNPL) if unpaid

APY vs APR What Is the Difference?

When banks and lenders quote interest rates, they use two different numbers:

APR (Annual Percentage Rate): The stated interest rate before compounding effects. Used mainly for loans and credit cards.

APY (Annual Percentage Yield): The effective annual rate after compounding is factored in. Used mainly for savings accounts.

| APR | APY | |

| Accounts for compounding | No | Yes |

| Used for | Loans, credit cards | Savings, CDs |

| Which is higher? | Lower number | Higher number |

| Which shows true cost/return? | No | Yes |

A savings account advertised at 5% APR with monthly compounding actually earns 5.12% APY. Always compare APY when evaluating savings products — it tells you your real rate of return.

How to Make Compound Interest Work for You

- Start as early as possible. Even small amounts invested in your 20s outperform large amounts invested in your 40s. Time is the biggest multiplier.

- Reinvest all earnings. Never withdraw interest or dividends. Let them compound. This is the key interrupt the cycle and you break the snowball.

- Increase compounding frequency. Choose accounts that compound daily or monthly over those that compound annually.

- Maximize tax-advantaged accounts first. In 401(k) and Roth IRA accounts, your compound growth is tax-deferred or tax-free supercharging the effect.

- Avoid high-interest debt. A 22% credit card APR compounding against you cancels out any 7% investment return you make simultaneously. Pay down high-interest debt first.

- Automate contributions. Monthly contributions alongside compound interest are a multiplier on top of a multiplier. Use our Compound Interest Calculator with Monthly Deposits to see the combined effect.

Frequently Asked Questions

What is compound interest in simple terms?

Compound interest means earning interest on your interest. Each time interest is added to your account, it becomes part of the balance that earns future interest creating snowball-like growth over time.

How is compound interest calculated?

Using the formula A = P × (1 + r/n)^(n×t), where P is your starting amount, r is the annual interest rate, n is how often interest compounds per year, and t is the number of years.

What is the difference between compound and simple interest?

Simple interest only applies to your original principal. Compound interest applies to your principal plus all previously earned interest. Over long periods, compound interest produces dramatically more growth.

Does compound interest really make a difference?

Yes significantly. $10,000 at 7% over 30 years earns $66,123 with compound interest versus $21,000 with simple interest. The longer the time period, the greater the difference.

What is the best account for compound interest?

High-yield savings accounts and CDs compound daily or monthly and are FDIC-insured. For long-term growth, tax-advantaged retirement accounts investing in index funds (401k, Roth IRA) typically produce higher returns through compound growth over decades.

Is compound interest the same as APY?

APY (Annual Percentage Yield) is the result of compounding applied to an APR over one year. It reflects what you actually earn. Compound interest is the mechanism APY is the resulting annual rate. Always compare APY between savings products.

Can compound interest make you rich?

It is one of the most reliable wealth-building tools available. $500 invested monthly at 8% for 35 years grows to approximately $1,000,000. The math works but it requires time, consistency, and leaving earnings to compound.